Table Of Contents

- What makes Africa a truly diverse and dynamic continent?

- What is digital identity?

- Why are digital national identity programs important for economic inclusion?

- What are some examples of successful digital ID programs?

- What challenges does Africa face while implementing digital national ID programs?

- How can digital national ID programs be implemented across Africa?

- Conclusion

What makes Africa a truly diverse and dynamic continent?

With a landmass that can fit in the US, India, Japan, Mexico and a few other EU countries, the sheer magnitude of Africa’s resources is truly inexplicable. Comprising 54 countries and over 3000 ethnic groups, Africa boasts a tapestry of languages, traditions, and histories. From the bustling markets of Marrakech to the savannahs of the Serengeti, the continent is a region of contrast and possibilities.

One of the most significant factors shaping Africa’s economic landscape is its population growth. With a current population of over 1.3 billion people, Africa is projected to reach 2.5 billion by 2050, making it the fastest-growing region in the world. Moreover, the continent’s youth population is booming, with over 60% of Africans under the age of 25. This demographic presents a unique opportunity for Africa to harness the energy and creativity of its young population.

Africa’s economic significance extends beyond its cultural and demographic diversity. Over the past decade, Africa’s GDP has been growing steadily, with a current average growth rate of around 3.8%. As Africa’s economy continues to evolve, it has the potential to become a major player in global markets.

While Africa’s economic growth and potential are promising, the continent also faces several challenges that must be addressed to fully unlock its opportunities. The informal nature of most African economies hinders access to basic services and job opportunities stagnating overall economic growth.

By formalising their economies, African governments and private organisations can empower populations, boost GDP growth, and improve health and well-being. This can be achieved through regulatory reforms, capacity-building initiatives, and leveraging technology for efficiency and transparency.

The formalisation of the economy empowers individuals by creating formal jobs, promoting entrepreneurship, and fostering skills development. It enhances the quality of life, reduces poverty, and stimulates economic growth. Additionally, this would also contribute to GDP growth by increasing tax revenues, attracting investments, stimulating innovation, and enhancing productivity. Governments and private organisations must collaborate and leverage technological advancements to bridge the digital divide, expand internet access, and promote digital literacy to drive economic formalisation and inclusive development in Africa.

What is digital identity?

Digital identity plays a crucial role in today’s advancing world, offering opportunities for accessing services and driving economic growth. It refers to proof of an individual’s identity that can be verified online and is issued by governments, organisations, or individuals. It consists of various information pieces like name, date of birth, ID number, and more, used for identification.

A well-planned digital identity system empowers underrepresented communities and contributes to economic growth. Digital economies already account for over 15% of global GDP, and trust-based ecosystems formed through efficient identity verification are key factors in propelling this growth. Digital identity also enables individuals from vulnerable regions to access essential rights and public services.

In contrast to digital identity systems, paper-based IDs, such as passports and driver’s licenses, contain personal information that requires physical inspection for verification. These IDs are prone to damage, loss, and theft and are less convenient for online activities. On the other hand, digital ID documents rely on advanced encryption and security protocols, protecting against fraud and identity theft. They can be easily accessed remotely through digital devices, offering greater convenience for online transactions and activities.

Why are digital national identity programs important for economic inclusion?

Digital national identity programs aim to provide citizens with a secure and reliable way to authenticate their identity. These programs typically involve the creation of a digital identity credential, such as a smart card, mobile app, or another form of digital token, that can be used to verify a user’s identity when accessing government services, making online purchases, or engaging in other digital transactions.

Digital IDs can also help governments reduce fraud and corruption, which can stimulate investment and economic activity by creating a more stable and predictable business environment. Additionally, digital IDs can help governments better target social safety net programs and subsidies, reducing waste and inefficiencies in government spending.

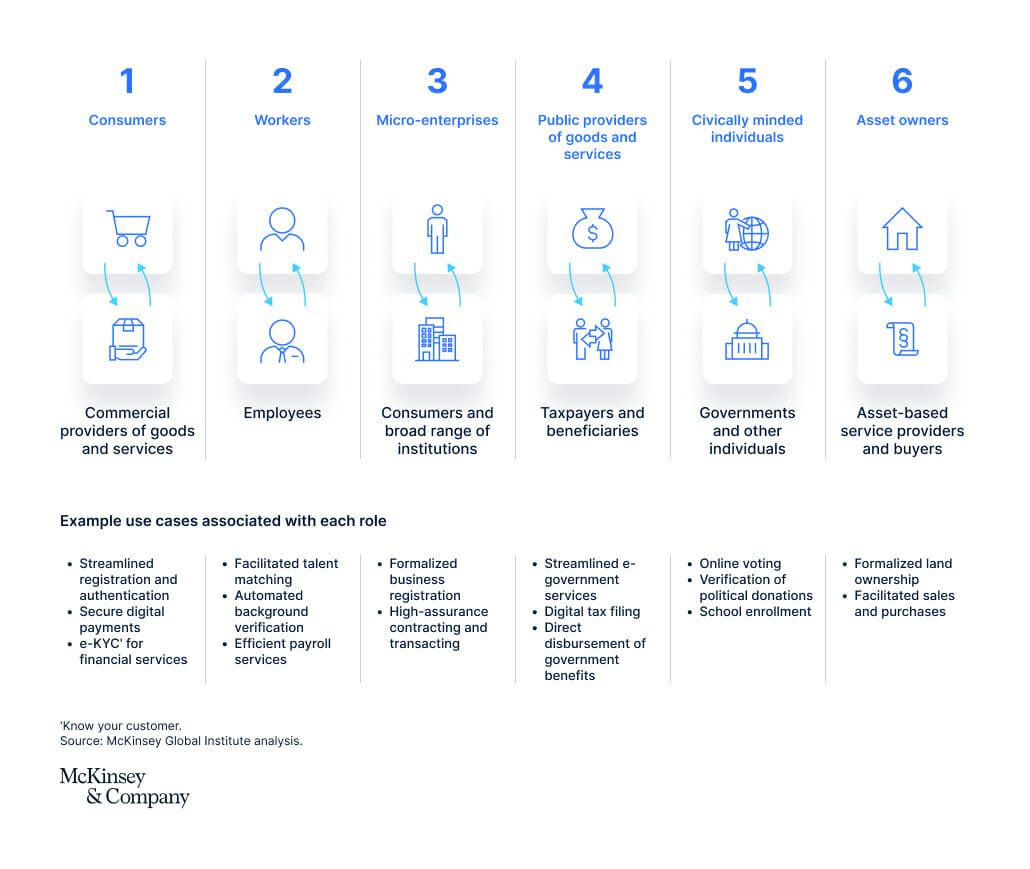

According to McKinsey, by 2030, digital identification could create economic value of up to $3.6 trillion globally. This includes both direct and indirect benefits, such as increased financial inclusion, reduced costs, and improved security and privacy.

When linked with digital payment systems, national IDs make public services more efficient. This enhances the accuracy of transactions, reduces the costs of doing business and identity frauds and also stimulates economic growth.

What are some examples of successful digital ID programs?

Digital national ID programs can provide a means for marginalised communities to obtain official identification documents, which can then be used to open bank accounts and access other financial services. Being direct and instantaneous, they can play a major role in enabling financial inclusion and providing greater access to basic services.

For example, in India, the “Aadhaar” digital identification program has enabled the government to distribute social welfare benefits more efficiently and reduced corruption in the distribution process. Launched in 2009, Aadhar assigns a unique identification number to each of the 1.2b citizens of India and uses biometric data to verify their identity.

By using “Aadhaar” to verify identity, the Indian government has been able to effectively distribute social welfare benefits, such as food and fuel subsidies to millions of eligible Indians. This has reduced fraud and leakage in the distribution process, resulting in significant cost savings for the government. In addition, Aadhaar has enabled greater financial inclusion by providing a means for citizens to access formal financial services, such as bank accounts and insurance, thereby impacting the lives of millions. This development has the potential to unlock 3-13% of GDP, according to estimates by McKinsey.

What challenges does Africa face while implementing digital national ID programs?

More than half a billion individuals in Africa lack an identity document, which has created an extensive barrier to accessing financial, healthcare, education and government services. This lack of identification creates a critical barrier to accessing financial services, with more than 30% of unidentified individuals facing difficulties in using financial services. This barrier is even more pronounced in marginalised sections of society, including women, migrants, rural communities and other vulnerable groups.

A major challenge African countries face while implementing digital identity systems is the fragmented landscape of the continent. With 54 countries each with its own unique political, social, and economic context, there is no one-size-fits-all solution that can be applied across the continent. Each country has its own unique identity systems, regulatory frameworks, and data protection laws, making it difficult to develop standardised approaches to digital identity.

Another challenge lies in the lack of adequate technological infrastructure in many African countries to support digital ID programs, especially in rural areas where access to digital resources is greatly limited.

Moreover, some African countries also face challenges related to political instability, conflicts, and human rights violations. This makes it difficult to establish the necessary legal and institutional frameworks needed to implement digital identity systems.

We have seen how India’s digital national ID program has been successful in addressing many of these challenges, and numerous lessons can be learned from these implementations in the context of Africa.

India and Africa have faced similar issues regarding digital transformation, which include low internet connectivity and a lack of digital infrastructure. With India’s rapidly growing digital economy, there is enormous potential for Africa to learn from India’s digital revolution. This includes the importance of having a robust institutional framework to support the development and implementation of a digital identity program. African countries would need to invest in developing a similar legal and institutional framework, as well as have clear guidelines for data privacy and security.

How can digital national ID programs be implemented across Africa?

Implementing digital national ID programs across Africa would require a joint effort by governments, private sector companies, and international organisations.

African countries would first have to leverage existing infrastructure, such as mobile networks and internet connectivity, to develop and implement digital national ID programs. This would help to minimise costs and ensure that the programs are accessible to a wide range of citizens. Along with this, legal and regulatory frameworks that define the collection, storage, and use of citizens’ data have to be established.

A key factor in implementing digital ID programs would involve building partnerships with private sector companies to minimise costs and build on their existing infrastructure. This would help bring in technical expertise while reducing overall costs.

Let’s look into a few examples of already in-place digital ID cards in Africa, and the key challenges they face.

1. ECOWAS Card:

A key example of a digital ID card in Africa is the ECOWAS Card, which lets individuals travel across the 16 ECOWAS states without a visa. The card has facilitated tourism, trade and cultural exchange among the member states. It also makes it easier for individuals to access services in these countries. Along with this, the ECOWAS ID card promotes a shared identity and enhances cooperation in various sectors, including security, agriculture, and infrastructure development.

One of the primary obstacles in implementing ECOWAS cards is ensuring consistent and effective implementation across all member countries. Each country has its own administrative procedures, infrastructure, and levels of digital readiness, which has often resulted in disparities in the issuance and recognition of ID cards. Harmonising these processes and establishing uniform standards can be complex and time-consuming.

uqudo’s digital infrastructure can help ECOWAS countries implement a standardised digital identity infrastructure that would support the exchange of data and uptake of products and services. This can be done using a combination of AI technology and alternative biometrics to create online identity profiles and connect people to a formal system.

2. M-Pesa

The M-Pesa card is a virtual card linked to a user’s M-Pesa account, allowing them to make payments and transactions at various merchants and withdraw cash from ATMs. It functions similarly to a debit card, where the cardholder can swipe or tap the card at point-of-sale (POS) terminals to make payments. It eliminates the need for carrying physical cash and enables individuals to manage their finances digitally.

Implementing the M-Pesa card has also faced numerous challenges, including the necessity of its acceptance in a wider network. For the card to be useful, it has to be accepted by a large number of merchants and businesses, which has been a hurdle in areas with limited access to technology and connectivity. Along with this, ensuring seamless cross-border transactions in the multiple countries M-Pesa operates is a complex affair.

uqudo’s scalable platform built on a cloud environment can facilitate cross-border transactions across the whole of Africa. Using a federated identity governments and enterprises across the continent can provide individuals with a seamless identity platform.

3. Voter ID Cards

Numerous African countries have a voter identification and registration system in place, but this process is often lengthy and cumbersome. In some countries, the entire process is poorly organised, leading to incomplete voter registration, which leads to excluding eligible voters in remote areas from the electoral process.

uqudo has a proven track record of conducting the first digital elections in Oman, which was the first-ever national election in the region. This demonstrates uqudo’s ability to provide reliable and secure digital identity solutions for critical use cases like elections. This can be replicated in the African continent to allow individuals to exercise their electoral rights.

Conclusion

Digital national identity programs have a profound impact on economic growth in Africa and emerging markets. By facilitating financial inclusion, streamlining access to products and services, improving government administration, and enhancing security, these programs create an enabling environment for economic development.

However, challenges such as infrastructure limitations, privacy concerns, inclusion issues, and political and regulatory hurdles need to be addressed to ensure the effective and inclusive implementation of these programs. Expanding coverage, strengthening data protection measures, fostering collaboration, and continuous evaluation is essential for maximising the positive impact of digital national ID programs on economic growth.

As Africa and emerging markets embrace the digital revolution, digital national ID programs serve as a catalyst for unlocking economic potential, empowering individuals, and creating a more inclusive and prosperous society.

Now that we have established the importance of a structured digital identity program, we will discuss more on the framework for implementing national IDs in the African continent in our next blog.