Know your customer (KYC) is the first fundamental step of customer identification and refers to the mandated process of identifying and verifying a customer’s identity. KYC involves numerous steps for validating a customer’s identity, understanding financial habits and verifying the legitimacy of funds.

KYC guidelines help industries stay protected against fraud, corruption, money laundering and terrorist financing activities. Though KYC procedures have been present since the 1990s, with a rise in money laundering and terrorist activities, the necessity of a stringent KYC program has been increasing in recent years.

The intensive use of technology has made KYC a lesser time-consuming process but has also made it easier for financial criminals to evade financial regulations. Due to this increase in organised crime, banks and other financial institutions have had to suffer the challenges of regulatory compliance.

Another essential factor that makes implementation of KYC in banking hard for financial institutions are the various document verification requirements in different regions. This global constraint of verification makes it necessary for financial institutions to have separate procedures for every country they operate in, in turn making KYC and AML compliance a lengthy and time-consuming process.

A large amount of data that has to be processed by companies performing KYC verification is another hassle for banks and financial institutions. While all data must be verified accurately for robust AML compliance, it is also necessary to keep the data secure as per legal regulations. This process, in turn, makes KYC and AML procedures tedious and complicated.

The cost associated with KYC in banking is another factor banks and financial institutions have to consider while developing KYC procedures. With costs mounting from internal processes that include transaction monitoring, external processes like background checks along with non-compliance fines, the total cost of KYC for banks and financial institutions is generally quite high. According to studies, the average cost of KYC procedures for banks and financial institutions is more than $60 million annually, and this does not include non-compliance fines.

Another important factor that necessitates a proper KYC compliance program is the growth of identity theft and cybercrime in the past decades. With growing cases of data breaches, having stringent KYC and screening procedures lies in the best interest of organizations.

Is KYC even necessary?

KYC refers to the verification of a customer’s identity and is generally considered a major component of an organization’s AML compliance procedure. Since it protects banks and financial institutions from money laundering, terrorist funding and other financial crimes, organizations today heavily invest in their own KYC procedures or outsource them from KYC/AML compliance firms.

To understand the importance of KYC, it is important to understand why AML/KYC regulations were first introduced. KYC regulations were first introduced in the 1990s by the FATF (Financial Action Task Force) and have been evolving since then. The implementation of KYC regulations became a necessity because of the growing cases of money laundering, tax evasion, terrorist funding and drug trafficking all over the world, which had a negative impact on the global economy.

A few key necessities of a regulated KYC procedure are:

- Reduces the occurrence of identity theft, due to a robust identity verification procedure.

- Decreases the occurrence of money laundering, tax evasion, terrorist funding, drug trafficking and other financial crimes.

- A detailed understanding of a customer’s financial activities helps banks serve them in a more customised manner.

- An adequately done risk assessment helps protect banks and financial institutions.

- A fully documented trail helps banks and financial institutions identify fraudsters in case of financial fraud.

- Helps stabilize a country’s economy and bring in foreign investments.

Why is KYC hard for banks and financial institutions?

Now that we have established the importance of a carefully regulated KYC program, we need to understand why banks and financial institutions have a hard time complying with KYC and AML rules. From different requirements in different countries to the difficulties faced by banks to keep their customer data safe from fraudsters, the proper implementation of KYC faces numerous challenges.

1. Differences in what KYC stands for in different businesses

One of the biggest challenges for organizations formulating KYC regulations is understanding the differences between Know your Customer and Know your Client. Both these procedures are fundamental in an organization’s AML compliance program, and despite their similarities, both their documentation requirements and verification procedures vary drastically.

Know your Customer is a procedure done by banks and other financial institutions while onboarding a new customer to their systems. This helps banks identify and verify their customers to ensure a customer is who they say they are supposed to be. KYC helps evaluate a customer’s risk profile, protecting banks and financial institutions from money laundering and other financial crimes.

Know your Client (also known as Know your Business – KYB) is a procedure done by banks, financial institutions and other organizations while establishing a relationship with a new client. This helps businesses identify the validity of the company they are doing business with, and ensure that they are dealing with legal entities and not shell companies.

How KYC and KYB solutions differ from each other, despite their equal importance in any business is the kind of level of verification required for each. Now, imagine you need to verify the identity of an individual. The kind of documents you will need for this would include a government-issued identity card and another document for address proof. You’ll also sometimes have to check if the given individual’s name is on any sanction list. That’s it!

Now imagine verifying the identity of a business. Obviously, verifying the identity of a company is a much more extensive process than doing that for an individual. For this, you will need a lot more documents than that for a much simpler KYC procedure. You will first need to check if the company actually exists and when was it legally formed. This is to ensure you’re actually dealing with a real company and not a shell one.

Since businesses have numerous top management personnel, you will next need to identify them and see if they fall under any restricted sanction lists. This is an important step because if a top-level employee of an organization has a high-risk potential, doing business with them is quite unsafe.

The reason why KYC and KYB are sometimes confusing for businesses is that they fail to recognize the key elements of both these procedures. Both these procedures require continuous due diligence, but the degree of this due diligence is more extensive while dealing with corporate organizations. And not to mention the variation of documents in each case, which bring us to the next point.

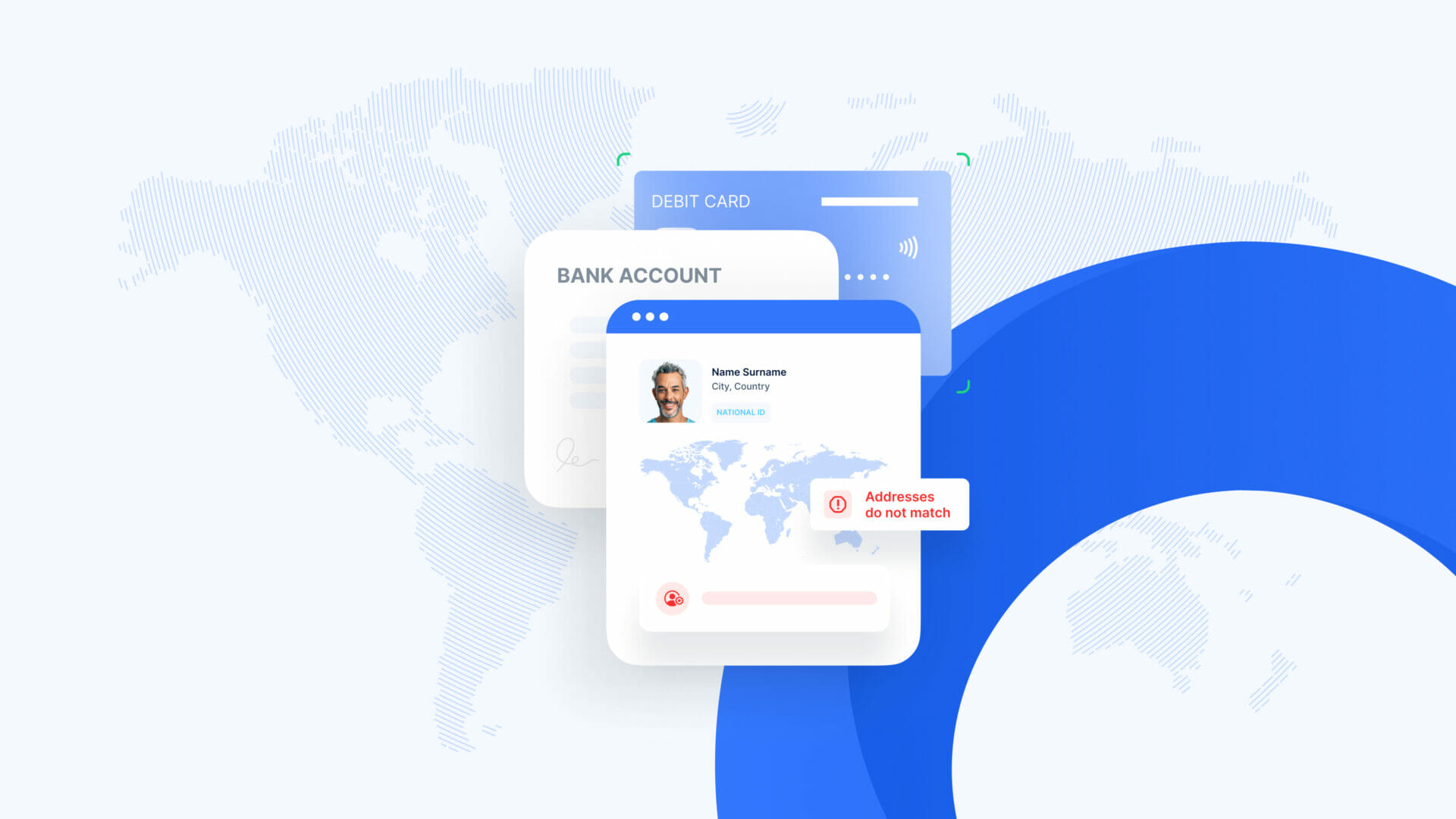

2. Variation of ID requirements for different regions

As established before, KYC involves the verification of documents of customers and businesses and is a key factor in an organization’s AML compliance. What makes this significantly difficult for banks and other financial institutions is the different ID/documentation requirements in different regions.

For example, in the UAE for KYC verification, a customer has to provide their Emirates ID. Along with this, some banks require individuals to provide address proof and a few other documents.

Similarly in the UK, an individual has to provide a valid passport, driving license or a national ID along with a separate identification document that contains address proof.

Now if we take into consideration the African countries, the online KYC verification process is even harder. With most African countries lacking any form of identification for their population, banks and other financial institutions find it very difficult to validate the identities of consumers. Some of these countries only have paper-based identification documents, and this makes it difficult for financial institutions to digitally verify them.

Imagine a key global firm with offices worldwide that has to verify individuals in the countries mentioned above. For doing this, it will have to curate a different verification procedure for each country, and then find ways to verify various kinds of identities while ensuring all different jurisdictions’ regulations are being followed. This cumbersome process is even more difficult for smaller firms with lesser funds.

3. Data privacy regulations

If someone had access to your phone they would be able to see everything on it, from pictures and conversations to your personal information like addresses and bank details. So in order to make all your personal data secure, you will have to ensure that your phone is protected from unauthorized access.

Similarly, when banks and other financial institutions obtain customer information from their KYC checks, it is very important that all this data is protected from fraudsters and criminals. Since stolen data from a KYC services portal can be misused tremendously, financial institutions have to ensure that all confidential information is very secure. Companies that perform due diligence checks on their customers regularly also need to ensure that all the data they collect is protected.

With legal entities levying hefty fines on companies that do not comply with data privacy regulations, it is very important for banks and financial institutions to have a clear process that protects their customers’ data. The GDPR (General Data Protection Regulation) regulates data protection and privacy in the EU region, and firms here have to strictly comply with it while dealing with customer data.

4. Hidden costs of KYC

The entire KYC process from customer identity verification to the mandatory ongoing checks is quite an expensive one for banks and other financial institutions. With some companies approximating a cost of around $370 million annually for KYC compliance, it is not surprising that financial institutions are increasing their KYC budgets.

Though it makes sense for large financial companies to spend greater funds on KYC/AML compliance, it is hard for smaller firms to heavily invest in them. Not only do companies need well-functioning KYC software, but they also need to spend funds training their staff on specific KYC guidelines and customer support.

Sometimes a lengthy KYC procedure leaves a customer dissatisfied, making them leave the process midway through. This customer dissatisfaction causes incalculable losses to banks and financial institutions. Not to mention that if the KYC process is too hard for customers (eg, asking for too many documents), it is often abandoned in the middle.

How can uqudo help your KYC procedures?

KYC is an essential process that plays a key role in protecting the financial interests of the banking systems.

As leading KYC solution providers in the region, uqudo’s simplified but efficient process solves all the problems mentioned above in the following manner:

1. Our fully customisable KYC and KYB procedures can access data from documents of over 248 countries with unparalleled accuracy. Our KYC platform use AI scanning services and face detection solutions to validate your customers’ details.

To establish and verify a business’s identity we screen from the world’s largest company and individuals’ lists to verify their authenticity. With access to the world’s largest global risk database, our KYB checks include those across monitored lists, PEPs and even adverse media.

2. uqudo’s customised document scanner can read and verify national ID documents of different countries according to each of their legal requirements, with document verification that can be done in milliseconds. Our liveness and selfie checks ensure that the individual is a real person and matches the documents being provided.

3. uqudo’s data collection is highly secure due to the usage of a powerful tech stack that ensures no data breaches can occur. Since uqudo provides fully automated KYC verification solutions, the possibility of manual error is absent. Our state-of-the-art biometric authentication and AI platform also minimise the risk of identity theft.

4. uqudo’s fully digitalised identity platform ensures secure data verification at minimal costs. Since we fully eliminate costs that arise from going to a bank in person and manual data verification, and other processing fees, our solutions are highly cost-effective, even for those with lesser investments.

uqudo’s rapid verification process not only ensures customer satisfaction but also reduces a company’s likelihood of being fined for non-KYC/AML compliance.

To schedule a call with us to enhance your KYC process, click here.